Please review and distribute as appropriate.

PURPOSE: The 89th Texas Legislature recently passed HB 4226 and SB 2064. The two bills add tax exemptions for certain motor vehicle transactions. Below is a brief summary of the changes and where to find additional information.

HB 4226 Effective September 1, 2025, Tax Code, Section 152.094, as amended by HB 4226, exempts the motor vehicle sales, use, and rental tax for the following:

- A motor vehicle purchased, used, or rented by a nonprofit food bank, and used primarily for the purpose of the food bank. A nonprofit food bank defined by Tax Code, Section 162.001(45-a), is a nonprofit entity that solicits, stores, and redistributes edible food to agencies that feed needy families and individuals

- A motor vehicle purchased, used, or rented by certain providers of housing and related services on motor vehicles used primarily to provide housing at locations they own or control. A provider of housing and related services is further described by Tax Code, Section 151.310(a). To qualify for the exemption, the housing provider must serve individuals experiencing homelessness with a disabling condition who have either been continuously homeless for at least one year or have had at least four episodes of homelessness in the past three years.

SB 2064 Effective September 1, 2025, SB 2064 introduces changes to the taxation of vehicles obtained through a decedent’s estate (inheritance).

- Motor vehicles inherited through a decedents estate or acquired by a rights of survivorship agreement are exempt from motor vehicle sales tax, which eliminates the $10.00 gift tax previously collected in these instances.

The tax exemptions enacted by HB 4226 and SB 2064 will apply to motor vehicle transfers, sales, uses, or rentals occurring on or after September 1, 2025.

Tax liabilities that accrued before the effective date of September 1, 2025, will still be governed by the former law.

Processing Tax Exemptions on or after September 1, 2025

Until further programming is implemented, tax exemptions may be processed in the following manner:

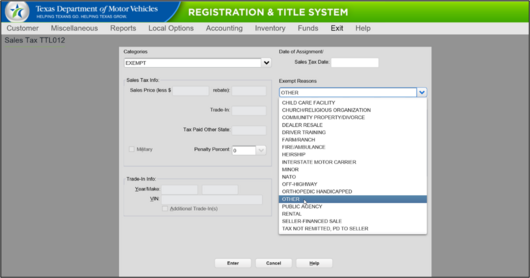

- Counties processing transactions in the Registration and Title System will need to select “Other” as the Exempt Reason on the Sales Tax TTL012 screen.

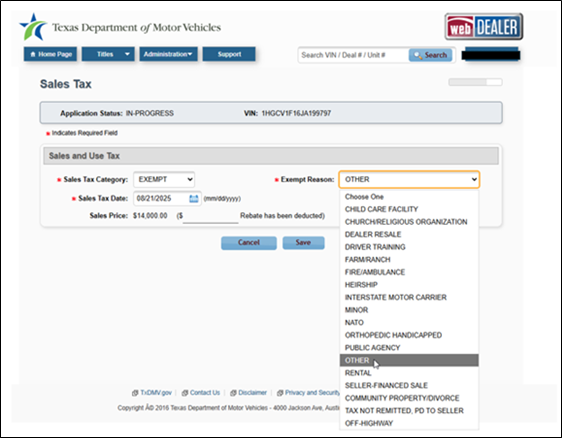

- Dealers processing transactions in webDEALER will need to select “Other” as the Exempt Reason on the Sales Tax screen.

Any future programming changes will be communicated with the applicable programming release. Stakeholders are encouraged to review HB 4226 and SB 2064 for more information. For specific questions regarding sales tax exemptions and qualifications, please contact the Comptroller of Public Accounts (CPA) at 800-252-5555.

If you have any questions, please contact your local TxDMV Regional Service Center.

Thank you,

Annette Quintero, Division Director

Vehicle Titles and Registration Division

Texas Department of Motor Vehicles

|